Firms often do not have the necessary data they need to draw a complete total cost curve for all levels of production. They cannot be sure of what total costs would look like if they, say, doubled production or cut production in half, because they have not tried it. Instead, firms experiment. They produce a slightly greater or lower quantity and observe how profits are affected. In economic terms, this practical approach to maximizing profits means looking at how changes in production affect marginal revenue and marginal cost.

Figure 8.3 presents the marginal revenue and marginal cost curves based on the total revenue and total cost in Table 8.1. The marginal revenue curve shows the additional revenue gained from selling one more unit. As mentioned before, a firm in perfect competition faces a perfectly elastic demand curve for its product—that is, the firm’s demand curve is a horizontal line drawn at the market price level. This also means that the firm’s marginal revenue curve is the same as the firm’s demand curve: Every time a consumer demands one more unit, the firm sells one more unit and revenue goes up by exactly the same amount equal to the market price. In this example, every time a pack of frozen raspberries is sold, the firm’s revenue increases by $4. Table 8.2 shows an example of this. This condition only holds for price taking firms in perfect competition where: marginal revenue = price.

The formula for marginal revenue is:

marginal revenue=change in total revenuechange in quantity

Table 8.2 Marginal Revenue

| Price | Quantity | Total Revenue | Marginal Revenue |

|---|---|---|---|

| $4 | 1 | $4 | – |

| $4 | 2 | $8 | $4 |

| $4 | 3 | $12 | $4 |

| $4 | 4 | $16 | $4 |

Notice that marginal revenue does not change as the firm produces more output. That is because the price is determined by supply and demand and does not change as the farmer produces more (keeping in mind that, due to the relative small size of each firm, increasing their supply has no impact on the total market supply where price is determined).

Since a perfectly competitive firm is a price taker, it can sell whatever quantity it wishes at the market-determined price. Marginal cost, the cost per additional unit sold, is calculated by dividing the change in total cost by the change in quantity. The formula for marginal cost is:

marginal cost=change in total costchange in quantity

Ordinarily, marginal cost changes as the firm produces a greater quantity.

In the raspberry farm example, shown in Figure 8.3, Figure 8.4 and Table 8.3, marginal cost at first declines as production increases from 10 to 20 to 30 packs of raspberries—which represents the area of increasing marginal returns that is not uncommon at low levels of production. But then marginal costs start to increase, displaying the typical pattern of diminishing marginal returns. If the firm is producing at a quantity where MR > MC, like 40 or 50 packs of raspberries, then it can increase profit by increasing output because the marginal revenue is exceeding the marginal cost. If the firm is producing at a quantity where MC > MR, like 90 or 100 packs, then it can increase profit by reducing output because the reductions in marginal cost will exceed the reductions in marginal revenue. The firm’s profit-maximizing choice of output will occur where MR = MC (or at a choice close to that point). You will notice that what occurs on the production side is exemplified on the cost side. This is referred to as duality.

Figure 8.3. Marginal Revenues and Marginal Costs at the Raspberry Farm: Individual Farmer. For a perfectly competitive firm, the marginal revenue (MR) curve is a horizontal straight line because it is equal to the price of the good, which is determined by the market, shown in Figure 8.4. The marginal cost (MC) curve is sometimes first downward-sloping, if there is a region of increasing marginal returns at low levels of output, but is eventually upward-sloping at higher levels of output as diminishing marginal returns kick in.

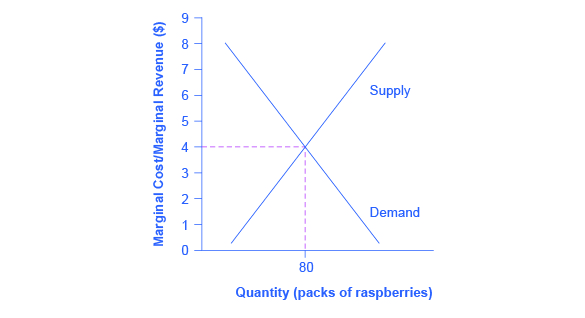

Figure 8.4. Marginal Revenues and Marginal Costs at the Raspberry Farm: Raspberry Market. The equilibrium price of raspberries is determined through the interaction of market supply and market demand at $4.00.

Table 8.3 Marginal Revenues and Marginal Costs at the Raspberry Farm

| Quantity | Total Cost | Fixed Cost | Variable Cost | Marginal Cost | Total Revenue | Marginal Revenue |

|---|---|---|---|---|---|---|

| 0 | $62 | $62 | – | – | – | – |

| 10 | $90 | $62 | $28 | $2.80 | $40 | $4.00 |

| 20 | $110 | $62 | $48 | $2.00 | $80 | $4.00 |

| 30 | $126 | $62 | $64 | $1.60 | $120 | $4.00 |

| 40 | $144 | $62 | $82 | $1.80 | $160 | $4.00 |

| 50 | $166 | $62 | $104 | $2.20 | $200 | $4.00 |

| 60 | $192 | $62 | $130 | $2.60 | $240 | $4.00 |

| 70 | $224 | $62 | $162 | $3.20 | $280 | $4.00 |

| 80 | $264 | $62 | $202 | $4.00 | $320 | $4.00 |

| 90 | $324 | $62 | $262 | $6.00 | $360 | $4.00 |

| 100 | $404 | $62 | $342 | $8.00 | $400 | $4.00 |

In this example, the marginal revenue and marginal cost curves cross at a price of $4 and a quantity of 80 produced. If the farmer started out producing at a level of 60, and then experimented with increasing production to 70, marginal revenues from the increase in production would exceed marginal costs—and so profits would rise. The farmer has an incentive to keep producing. From a level of 70 to 80, marginal cost and marginal revenue are equal so profit doesn’t change. If the farmer then experimented further with increasing production from 80 to 90, he would find that marginal costs from the increase in production are greater than marginal revenues, and so profits would decline.

The profit-maximizing choice for a perfectly competitive firm will occur where marginal revenue is equal to marginal cost—that is, where MR = MC. A profit-seeking firm should keep expanding production as long as MR > MC. But at the level of output where MR = MC, the firm should recognize that it has achieved the highest possible level of economic profits. (In the example above, the profit maximizing output level is between 70 and 80 units of output, but the firm will not know they’ve maximized profit until they reach 80, where MR = MC.) Expanding production into the zone where MR < MC will only reduce economic profits. Because the marginal revenue received by a perfectly competitive firm is equal to the price P, so that P = MR, the profit-maximizing rule for a perfectly competitive firm can also be written as a recommendation to produce at the quantity where P = MC.