The monopolistically competitive firm decides on its profit-maximizing quantity and price in much the same way as a monopolist. A monopolistic competitor, like a monopolist, faces a downward-sloping demand curve, and so it will choose some combination of price and quantity along its perceived demand curve.

As an example of a profit-maximizing monopolistic competitor, consider the Authentic Chinese Pizza store, which serves pizza with cheese, sweet and sour sauce, and your choice of vegetables and meats. Although Authentic Chinese Pizza must compete against other pizza businesses and restaurants, it has a differentiated product. The firm’s perceived demand curve is downward sloping, as shown in Figure 10.3 and the first two columns of Table 10.1.

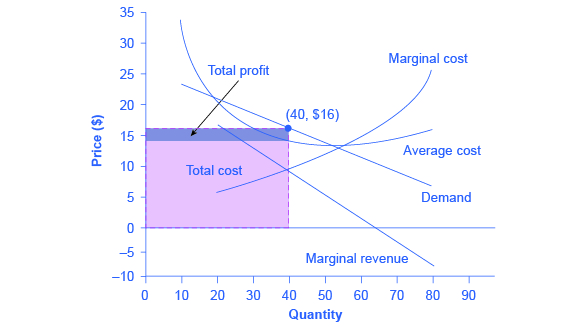

Figure 10.3. How a Monopolistic Competitor Chooses its Profit Maximizing Output and Price To maximize profits, the Authentic Chinese Pizza shop would choose a quantity where marginal revenue equals marginal cost, or Q where MR = MC. Here it would choose a quantity of 40 and a price of $16.

| Table 10.1. Revenue and Cost Schedule | ||||||

|---|---|---|---|---|---|---|

| Quantity | Price | Total Revenue | Marginal Revenue | Total Cost | Marginal Cost | Average Cost |

| 10 | $23 | $230 | — | $340 | – | $34 |

| 20 | $20 | $400 | $17 | $400 | $6 | $20 |

| 30 | $18 | $540 | $14 | $480 | $8 | $16 |

| 40 | $16 | $640 | $10 | $580 | $10 | $14.50 |

| 50 | $14 | $700 | $6 | $700 | $12 | $14 |

| 60 | $12 | $720 | $2 | $840 | $14 | $14 |

| 70 | $10 | $700 | –$2 | $1,020 | $18 | $14.57 |

| 80 | $8 | $640 | –$6 | $1,280 | $26 | $16 |

The combinations of price and quantity at each point on the demand curve can be multiplied to calculate the total revenue that the firm would receive, which is shown in the third column of Table 10.1. The fourth column, marginal revenue, is calculated as the change in total revenue divided by the change in quantity. The final columns of Table 10.1 show total cost, marginal cost, and average cost. As always, marginal cost is calculated by dividing the change in total cost by the change in quantity, while average cost is calculated by dividing total cost by quantity. The following example shows how these firms calculate how much of its product to supply at what price.